The Bitcoin "IPO Era" has arrived: Sideways movement is not the end, but the beginning of accumulation.

Bitcoin’s ongoing price consolidation signals the arrival of its “IPO moment.” Why does this mark a new era of higher asset allocation? Here’s the explanation.

Jordi Visser’s recent article tackles a crucial question: despite a constant flow of bullish developments—robust ETF inflows, major regulatory advancements, and rising institutional interest—Bitcoin’s trading remains stubbornly range-bound.

Visser argues that Bitcoin is undergoing a “silent IPO,” evolving from a “fantasy concept” into a “mainstream success story.” Typically, stocks in this phase consolidate for 6 to 18 months before resuming an upward trend.

Consider Facebook (now Meta) as an example. On May 12, 2012, Facebook debuted at $38 per share. For over a year, its share price fluctuated and declined, unable to break past its IPO price for 15 months. Google and other high-profile tech startups have shown similar patterns in their initial public periods.

Visser emphasizes that price consolidation isn’t necessarily a sign of trouble for the asset itself. This pattern often reflects founders and early employees choosing to “cash out.” Those who took high risks in the company’s early days and gained outsized returns naturally want to secure profits. The process of insider selling and institutional accumulation takes time—only after ownership transfers reach equilibrium will prices resume their upward trajectory.

Visser notes striking parallels with Bitcoin’s current state. Early adopters—who entered at $1, $10, $100, or $1,000—now possess generational wealth. Bitcoin has now “entered the mainstream”—ETFs are listed on the NYSE, major corporations hold it as reserves, and sovereign wealth funds are participating—giving early investors the opportunity to realize gains.

This is worth celebrating—their patience has been rewarded. Five years ago, selling $1 billion in Bitcoin could have disrupted the market; today, greater buyer diversity and trading volume now allow the market to absorb large transactions more smoothly.

It’s important to note that on-chain data interpretations of “who is selling” vary, so Visser’s analysis is just one factor affecting market trends. Nevertheless, this factor is pivotal and merits close attention for its potential impact on future markets.

Here are two key takeaways I’ve drawn from the article.

Conclusion 1: The Long-Term Outlook Is Exceptionally Bullish

Many crypto investors react to Visser’s article with disappointment: “Early whales are selling Bitcoin to institutions! Do they know something we don’t?”

This interpretation is completely mistaken.

Early investor selling doesn’t signal the “end of life” for an asset; it marks the beginning of a new phase.

Consider Facebook again. While its shares traded below $38 for a year after its IPO, today they trade at $637—up 1,576% from the IPO price. If I could return to 2012, I’d gladly buy Facebook stock at $38 per share.

Of course, a Series A investment would have produced higher returns—though with far greater risk than post-IPO.

Bitcoin is in a comparable position. While hundredfold annual returns will be less likely in the future, once the phase of widespread asset allocation ends, significant upside remains. The Bitwise Bitcoin Long-Term Capital Market Assumptions report forecasts Bitcoin reaching $1.3 million per coin by 2035—a prediction I consider conservative.

There’s also a key distinction: after an IPO, companies must continue growing to support their share price—Facebook couldn’t leap from $38 to $637 overnight, lacking the revenue and profit to justify such gains, and had to expand and innovate, which involved risk.

Bitcoin differs—once early whales finish selling, it doesn’t need to “do anything.” To move from a $2.5 trillion market cap to gold’s $25 trillion, Bitcoin needs only “broad acceptance.”

While this won’t happen instantly, Bitcoin’s appreciation cycle may unfold faster than Facebook’s.

Viewed long-term, Bitcoin’s price consolidation is a “golden opportunity.” I believe it’s the ideal moment to accumulate before the next rally.

Conclusion 2: The Era of 1% Bitcoin Allocation Is Over

As Visser highlights, post-IPO companies are less risky than startups—their equity is more distributed, regulatory oversight is stronger, and diversification opportunities are greater. Investing in Facebook post-IPO is far safer than backing a Silicon Valley startup founded by college dropouts in a party house.

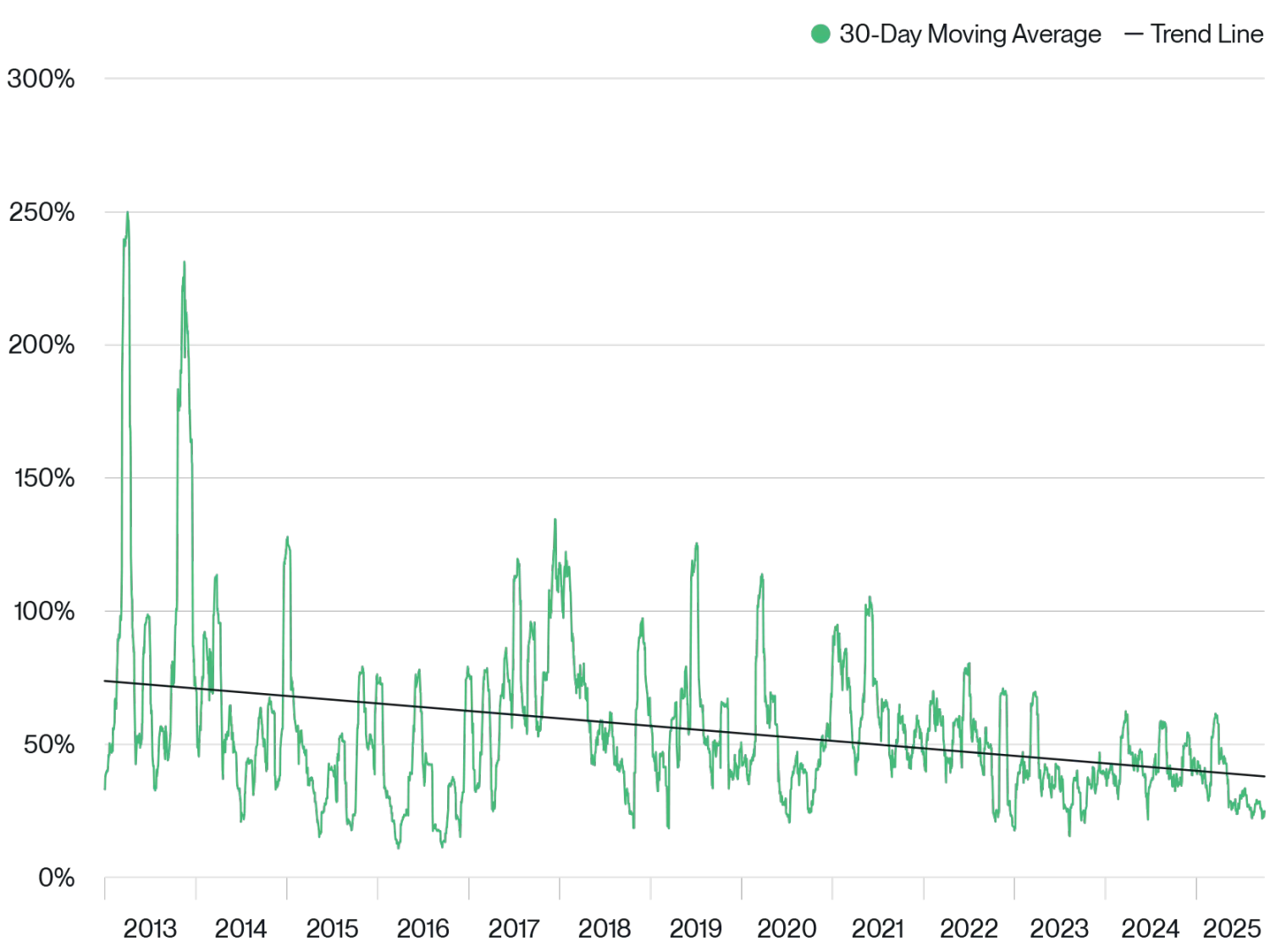

Bitcoin is in a parallel phase. With holders shifting from “early enthusiasts” to “institutional investors,” and with maturing technology, Bitcoin no longer faces existential risk. It’s now a mature asset class. This is evident in its volatility—since Bitcoin ETFs launched in January 2024, volatility has dropped sharply.

Bitcoin Historical Volatility

Source: Bitwise Asset Management. Data range: January 1, 2013 to September 30, 2025.

This transition delivers a key insight to investors: future Bitcoin returns may dip slightly, but volatility will decrease substantially. As an asset allocator, I’m not selling—in fact, with Bitcoin expected to be among the top-performing global assets in the next decade—I’m increasing my position.

Put simply, lower volatility means “it’s less risky to hold a larger allocation.”

Visser’s article validates a trend we’ve seen firsthand: in recent months, Bitwise has held hundreds of meetings with advisors, institutions, and professional investors, observing a clear shift—the era of a 1% Bitcoin allocation is over. More investors are treating 5% as the new baseline.

Bitcoin is living its “IPO moment.” If history is a guide, increasing exposure is the way to embrace this new era.

Disclaimer:

- This article is reproduced from [Foresight News] with copyright belonging to the original author [Matt Hougan, Bitwise Chief Investment Officer]. For republication concerns, please contact the Gate Learn team for prompt resolution.

- Disclaimer: The views and opinions in this article are those of the author and do not constitute investment advice.

- Other language versions of this article are translated by the Gate Learn team. Do not copy, distribute, or plagiarize the translated content without acknowledgment of Gate.

Share

Content

Related Articles

In-depth Explanation of Yala: Building a Modular DeFi Yield Aggregator with $YU Stablecoin as a Medium

BTC and Projects in The BRC-20 Ecosystem

What Is a Cold Wallet?

Blockchain Profitability & Issuance - Does It Matter?

Notcoin & UXLINK: On-chain Data Comparison