#GlobalRate-CutExpectationsCoolOff

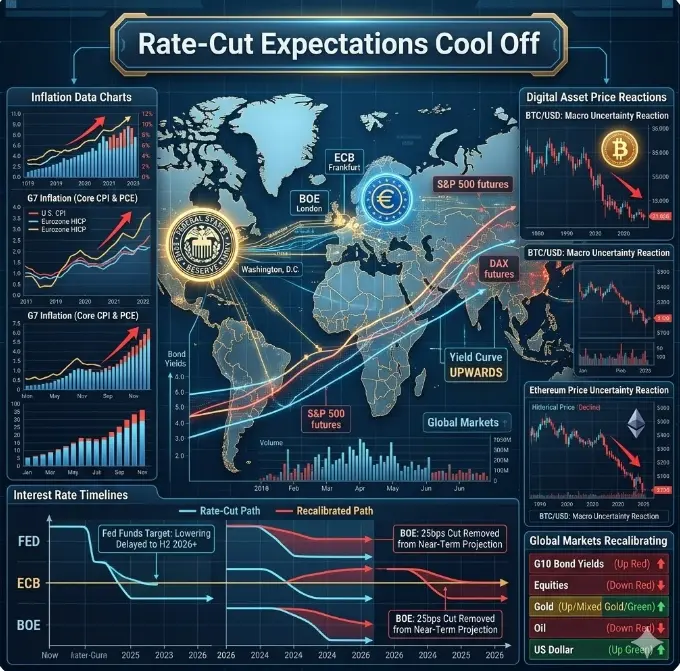

Global financial markets have recently shifted their expectations around interest rate policy as new economic data has reduced the probability of imminent rate cuts by central banks. After a period in which inflation showed signs of slowing and labor markets softened, investors had priced in multiple rate cuts from major central banks — including the Federal Reserve, the European Central Bank, and others. However, the latest macroeconomic indicators and policy signals suggest that those expectations are now being recalibrated, leading to a “rate‑cut cool‑off” across global markets.

Why Rate‑Cut Expectations Cooled

The shift stems from a mix of stronger‑than‑anticipated economic readings in key regions:

Resilient Inflation Data

Recent CPI and PCE inflation readings in the U.S. and Europe remained stickier than markets had hoped. Even as price pressures eased from their multi‑year highs, core inflation components — especially services and shelter costs — have continued to surprise to the upside. This reduces urgency for policymakers to lower policy rates.

Strong Employment Metrics

Labor market data has remained robust in several advanced economies. While some reports showed slight slowing, unemployment rates have held near cyclical lows, supporting consumer spending and economic growth. When employment stays strong, central banks typically avoid cutting rates prematurely for fear of reigniting inflation pressures.

Credit Conditions & Consumer Spending

Credit demand and bank lending surveys indicate that credit conditions are not loosening rapidly. Coupled with continued consumer spending, this suggests that aggregate demand remains healthy — another reason policymakers may delay easing measures.

Divergences Among Central Banks

Notably, while emerging market central banks have begun modest rate reductions as inflation falls closer to targets, major developed‑market central banks are taking a more cautious stance. For example, the Fed’s messaging — emphasizing patience and data dependency — has continued to discourage aggressive easing bets.

Market Reaction: Repricing in Real Time

The immediate reaction in global markets has been visible across key asset classes:

Bond Yields Risen: Expectations for rate cuts were priced heavily into bond markets over recent months. With cooling expectations, yields on 2‑year and 10‑year Treasuries have climbed, reflecting a lower probability of near‑term Fed easing.

Equities Taking a Breather: Risk assets such as stocks and cryptocurrencies rallied when rate‑cut expectations rose. But as markets recalibrated, some of those gains have moderated, especially in rate‑sensitive sectors like technology.

FX Volatility: Currencies perceived as “carry trades” or tied to higher yielding economies have shown strength, as traders reduce bets on lower global rates.

According to Dragon Fly Official, this repricing reflects a more nuanced understanding of macro fundamentals. The market learned that while inflation has eased from crisis‑era extremes, it is not yet at levels that guarantee sustained policy accommodation. As a result, the potential for multiple rate cuts in 2026 — once widely anticipated — is now significantly reduced.

Implications for Crypto and Risk Assets

In the context of digital assets, cooling rate‑cut expectations matter because:

Liquidity Premium Drops: Cryptocurrencies are often buoyed during periods of abundant liquidity. With rate cuts deferred, risk capital may remain more selective.

Correlation with Equities: Crypto markets have shown stronger correlation with U.S. equities in recent cycles. As equities adjust to the new pricing regime, crypto could similarly face sideways or corrective phases.

Macro Sentiment Shift: Investor sentiment tends to favor risk assets when real yields decline. If yields stabilize or rise modestly, risk‑off rotations could intensify.

However, it’s important to recognize that markets are dynamic. Even as expectations cool now, a future economic slowdown or renewed inflation decline could bring rate‑cut pricing back into focus.

What to Watch Next

Dragon Fly Official highlights several key data points and events that could influence the next phase of monetary policy expectations:

Upcoming CPI and PCE prints for the U.S. and eurozone

Central bank meeting minutes and speeches from key policymakers

Labor market and consumer confidence indicators

Credit growth and lending conditions surveys

These metrics will be critical in assessing whether rate‑cut expectations stabilize, continue to cool, or eventually reverse.

Bottom Line

The recent cooling in global rate‑cut expectations is not necessarily bearish for all markets, but it is a signal that investors are reassessing the pace and probability of monetary easing. This recalibration reflects stronger underlying economic data and cautious messaging from central banks — especially in developed markets. As the macro backdrop evolves, markets will continue to balance growth, inflation, and policy risk.

For now, the narrative has shifted from “imminent easing” to “data dependency and patience” — and that shift may be the defining macro theme of the current cycle.

Global financial markets have recently shifted their expectations around interest rate policy as new economic data has reduced the probability of imminent rate cuts by central banks. After a period in which inflation showed signs of slowing and labor markets softened, investors had priced in multiple rate cuts from major central banks — including the Federal Reserve, the European Central Bank, and others. However, the latest macroeconomic indicators and policy signals suggest that those expectations are now being recalibrated, leading to a “rate‑cut cool‑off” across global markets.

Why Rate‑Cut Expectations Cooled

The shift stems from a mix of stronger‑than‑anticipated economic readings in key regions:

Resilient Inflation Data

Recent CPI and PCE inflation readings in the U.S. and Europe remained stickier than markets had hoped. Even as price pressures eased from their multi‑year highs, core inflation components — especially services and shelter costs — have continued to surprise to the upside. This reduces urgency for policymakers to lower policy rates.

Strong Employment Metrics

Labor market data has remained robust in several advanced economies. While some reports showed slight slowing, unemployment rates have held near cyclical lows, supporting consumer spending and economic growth. When employment stays strong, central banks typically avoid cutting rates prematurely for fear of reigniting inflation pressures.

Credit Conditions & Consumer Spending

Credit demand and bank lending surveys indicate that credit conditions are not loosening rapidly. Coupled with continued consumer spending, this suggests that aggregate demand remains healthy — another reason policymakers may delay easing measures.

Divergences Among Central Banks

Notably, while emerging market central banks have begun modest rate reductions as inflation falls closer to targets, major developed‑market central banks are taking a more cautious stance. For example, the Fed’s messaging — emphasizing patience and data dependency — has continued to discourage aggressive easing bets.

Market Reaction: Repricing in Real Time

The immediate reaction in global markets has been visible across key asset classes:

Bond Yields Risen: Expectations for rate cuts were priced heavily into bond markets over recent months. With cooling expectations, yields on 2‑year and 10‑year Treasuries have climbed, reflecting a lower probability of near‑term Fed easing.

Equities Taking a Breather: Risk assets such as stocks and cryptocurrencies rallied when rate‑cut expectations rose. But as markets recalibrated, some of those gains have moderated, especially in rate‑sensitive sectors like technology.

FX Volatility: Currencies perceived as “carry trades” or tied to higher yielding economies have shown strength, as traders reduce bets on lower global rates.

According to Dragon Fly Official, this repricing reflects a more nuanced understanding of macro fundamentals. The market learned that while inflation has eased from crisis‑era extremes, it is not yet at levels that guarantee sustained policy accommodation. As a result, the potential for multiple rate cuts in 2026 — once widely anticipated — is now significantly reduced.

Implications for Crypto and Risk Assets

In the context of digital assets, cooling rate‑cut expectations matter because:

Liquidity Premium Drops: Cryptocurrencies are often buoyed during periods of abundant liquidity. With rate cuts deferred, risk capital may remain more selective.

Correlation with Equities: Crypto markets have shown stronger correlation with U.S. equities in recent cycles. As equities adjust to the new pricing regime, crypto could similarly face sideways or corrective phases.

Macro Sentiment Shift: Investor sentiment tends to favor risk assets when real yields decline. If yields stabilize or rise modestly, risk‑off rotations could intensify.

However, it’s important to recognize that markets are dynamic. Even as expectations cool now, a future economic slowdown or renewed inflation decline could bring rate‑cut pricing back into focus.

What to Watch Next

Dragon Fly Official highlights several key data points and events that could influence the next phase of monetary policy expectations:

Upcoming CPI and PCE prints for the U.S. and eurozone

Central bank meeting minutes and speeches from key policymakers

Labor market and consumer confidence indicators

Credit growth and lending conditions surveys

These metrics will be critical in assessing whether rate‑cut expectations stabilize, continue to cool, or eventually reverse.

Bottom Line

The recent cooling in global rate‑cut expectations is not necessarily bearish for all markets, but it is a signal that investors are reassessing the pace and probability of monetary easing. This recalibration reflects stronger underlying economic data and cautious messaging from central banks — especially in developed markets. As the macro backdrop evolves, markets will continue to balance growth, inflation, and policy risk.

For now, the narrative has shifted from “imminent easing” to “data dependency and patience” — and that shift may be the defining macro theme of the current cycle.